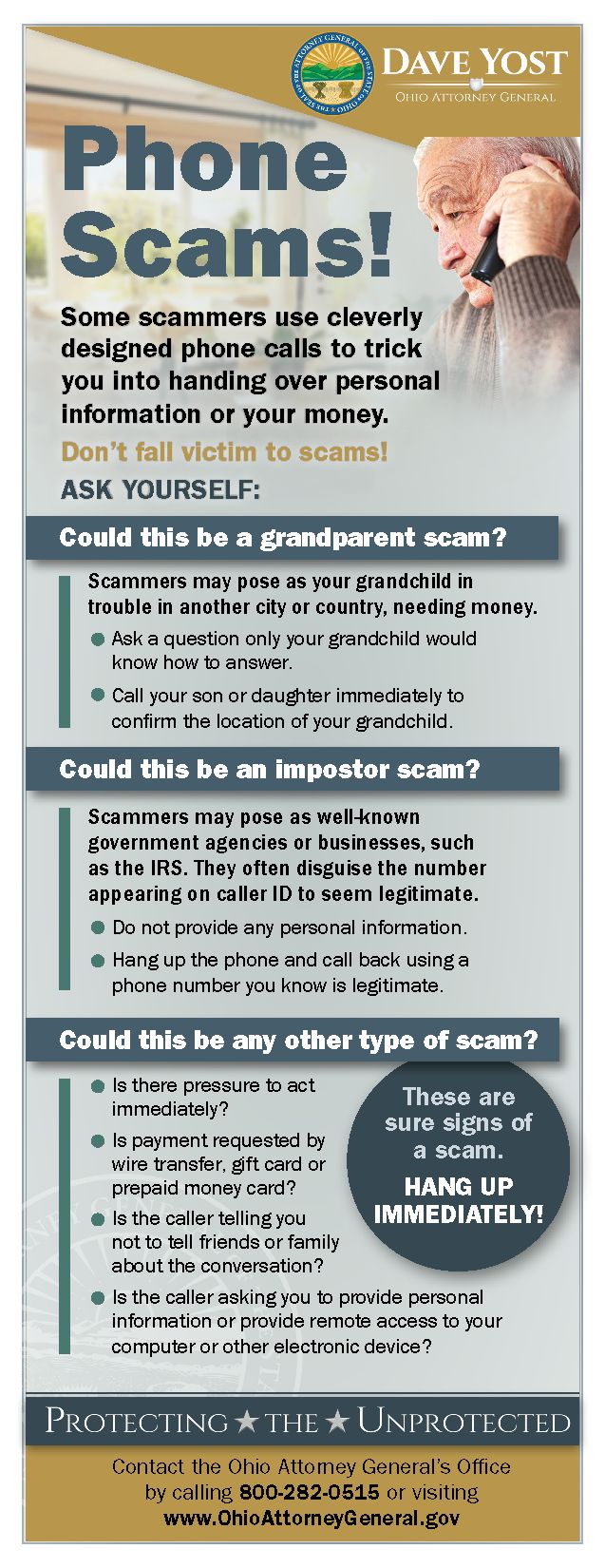

A credit freeze sounds like something people do after a disaster. In reality, it is closer to locking the front door before leaving the house. It does not fix every identity theft risk, and it does not watch your checking account for strange charges, but it can make it harder for someone to open a new credit account in your name.

That distinction matters because many households treat identity protection like a single switch. They freeze their credit and assume the job is done. Or they sign up for a monitoring service and assume a freeze is unnecessary. Neither habit is quite right. A freeze and monitoring do different jobs, and a family that understands the difference can avoid both panic and false comfort.

So what does a credit freeze actually do? It limits access to your credit report. If a lender cannot check the report, it usually will not approve a new credit card, loan, or financing account. That is why a freeze can be useful after a data breach, a stolen wallet, suspicious mail, or any moment when a Social Security number may have been exposed.

The freeze is free at the three major credit bureaus. It is also free to lift. That matters for people who remember the older days when freezing credit could feel like a paid add-on or an emergency-only step. The modern version is more practical. You can freeze your file, keep the freeze in place, and temporarily lift it when you actually need a lender, landlord, insurer, or cell-phone company to check credit.

Where people get tripped up is existing accounts. A credit freeze usually does not stop fraud on a card, bank account, payment app, or loan that already exists. If someone has your debit card number, a freeze will not make the card stop working. If a criminal gets into an online banking login, the freeze will not throw them out. That is why account alerts and regular statement checks still matter.

There is a second misunderstanding: a freeze is not the same as a fraud alert. A fraud alert tells businesses to take extra steps before opening new credit in your name. A freeze is stronger because it restricts access to the report. A fraud alert can be useful if you want a lighter step, especially after a possible exposure, but a freeze is often the cleaner move when the household wants to reduce new-account risk.

Should everyone keep a freeze on all the time? For many people, yes, especially if they are not actively applying for credit. A retiree who is not shopping for a mortgage, car loan, new card, or apartment may lose very little convenience by keeping a freeze in place. A younger household that applies for credit more often may need to manage temporary lifts, but even then, the process is usually not difficult once the accounts are set up.

The chore is that there are multiple places to manage. Freezing one bureau is not enough. A careful household freezes with Equifax, Experian, and TransUnion, saves the login information in a password manager, and writes down the process for temporarily lifting each freeze. If a couple manages finances together, both spouses may need their own freezes. Children can have credit files too, and child identity theft can stay hidden for years.

What about credit monitoring? Monitoring is useful after the fact. It can alert you when something changes, such as a new account, inquiry, or balance movement. But monitoring is not prevention by itself. If the alert arrives after a fraudulent account has already been opened, the household still has to dispute it. The best setup uses a freeze to reduce new-account approvals and monitoring or manual checks to catch what still gets through.

A practical routine is simple. Freeze the reports. Turn on transaction alerts for checking accounts and credit cards. Use unique passwords and two-factor authentication on financial accounts. Review credit reports through AnnualCreditReport.com. Check mailed notices instead of assuming they are junk. And when a company announces a breach, do not wait for perfect information before locking down credit.

What should you do before lifting a freeze? Ask the lender which credit bureau it plans to use and how long the lift needs to last. Some applications need only one bureau. Others may pull more than one. A temporary lift for a few days is usually safer than removing the freeze entirely and forgetting to restore it.

The best identity-theft plan is not dramatic. It is boring and layered. A freeze reduces one door. Account alerts watch another. Strong passwords protect another. Statements catch the things no app can explain for you. That is the rhythm households need, especially when more financial life now happens through email links, phones, and old passwords people have reused for years.

What is the sanity check before acting? Put the decision into one sentence and one dollar amount. If the sentence sounds vague, the household is probably not ready. For example: we are freezing credit to reduce new-account fraud risk; we are locking this cash for six months because the tax bill is not due until then; we are limiting income this year because Medicare premiums could change; we are rolling over this account because the new option is cheaper and easier to manage. A clear sentence exposes weak reasoning fast.

What would make this choice wrong? Every financial move has a failure point. The account could charge a fee that was buried in the disclosure. A benefit rule could change after income crosses a line. A bank product could renew automatically. A rollover could land in the wrong account type. A security step could protect new credit but not the card already in a wallet. Writing down the failure point makes the decision less emotional and easier to revisit.

The useful move is not to turn a money decision into a homework project that never ends. It is to pull the actual statement, plan notice, account agreement, or government page and write down the one number that changes the household decision. That might be the monthly payment, the interest rate, the tax bracket, the deductible, the income threshold, or the date when a rule changes. A lot of expensive mistakes start when people discuss money in general terms instead of looking at the document in front of them.

There is also a timing problem. A choice that looks fine in July can feel different in November if a spouse retires, a car breaks down, a prescription changes, or a child needs help. Before moving money, signing up for a new account, or choosing a benefit option, households should ask what happens if income is lower for two months or expenses are higher than expected. The boring answer is often the safest one: keep enough flexibility that one surprise does not force the next bad decision.

A second pass should be boring on purpose. Check the name on the account, the tax year, the beneficiary, the insurance limit, the renewal date, the password, and the exact dollar amount. People rarely make one giant mistake out of nowhere. More often, they stack three small assumptions, then wonder why the result feels wrong. The second pass catches those assumptions before they become paperwork.

If a spouse, adult child, or trusted helper is involved, the household should make the decision understandable to that person too. A plan that only one person can explain is fragile. The next emergency may happen when that person is sick, traveling, grieving, or busy. A short note with the account name, reason for the move, deadline, and source page can save the family from guessing later.

The final check is whether the decision still makes sense if conditions change a little. If one lower paycheck, one missed renewal notice, one higher premium, or one delayed transfer would turn the move into a problem, the plan is too tight. Good household finance usually leaves a margin. That margin may not look impressive in a spreadsheet, but it protects sleep, options, and relationships. The household should be able to explain not only why the move looks good today, but why it remains survivable if the first assumption turns out to be wrong. That is the difference between a clever money move and a durable one. If the choice cannot survive a modest surprise, the household should either shrink the move, wait, or keep more cash available before committing.

None of this means people should avoid every change. Better rates, lower fees, safer accounts, and smarter benefit choices can make a real difference. The point is to move one step at a time and keep a record. Save the disclosure. Screenshot the rate. Write down the phone call date. If a bank, insurer, employer, or government agency gives different answers later, that paper trail can save hours of stress.

For educational purposes only. This is general information, not personal financial, tax, legal, insurance, or investment advice. A household with a complicated tax return, health situation, debt problem, or retirement decision should consider speaking with a qualified professional before acting. Rules can change, thresholds can move, and small facts can change the answer. When money, taxes, credit, insurance, or retirement benefits are involved, the final decision should be based on current, official documents, not memory, rumor, old assumptions, shortcuts, guesses, stale notes, or a social media summary.

Sources: FTC: Credit freezes and fraud alerts; Consumer Financial Protection Bureau: Fraud alerts and security freezes; AnnualCreditReport.com.